Retirees with limited assets face the specter of outliving them. The only assurance offered by investment advisors that this will not happen is application of what is called the 4% rule. The rule says that if the retiree draws 4% of his assets every year and increases the draw amount by 4% every year, the assets will outlive him. There is no logic behind the rule, its rationale is that over a wide range of simulations of asset returns, it works.

This article does not question whether or not the 4% rule is 100% safe. Rather, it argues that there is an alternative that is equally safe, if not more so, while generating larger monthly draws. The alternative is the asset/annuity combo, where part of the assets is used to purchase a deferred annuity and the remainder is used for draw amounts during the deferment period. The combo uses an ingenious method developed by my colleague Allan Redstone to splice the two sources.

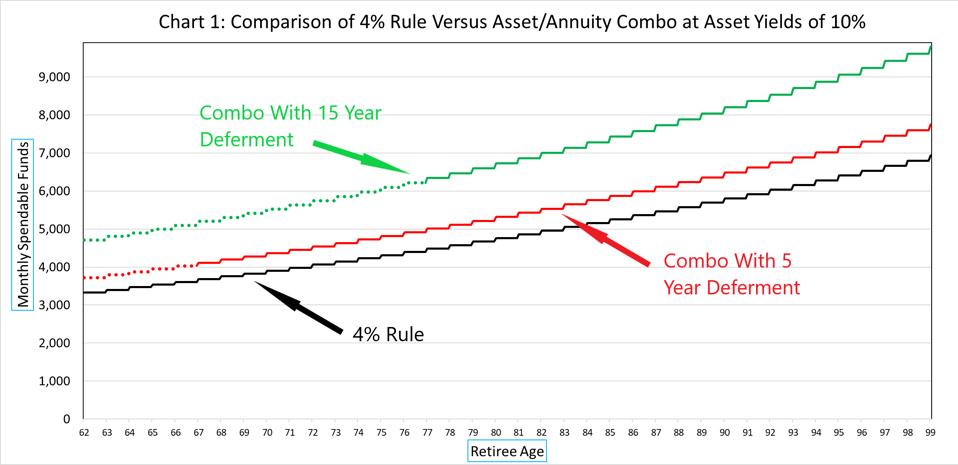

Combos will be compared to the 4% rule for a retiree of 62 who is assumed to live to 104. The draws from all combos are set to increase by 2% per year. To cover a wide range of possibilities, I use asset yields of 2% and 10%, and deferment periods of 5 years and 15 years. Chart 1 uses the 10% yield. The dotted part of the combo lines indicates asset draws while the solid line is annuity payments. The combo in both cases works better than the 4% rule.

www.mtgprofessor.com

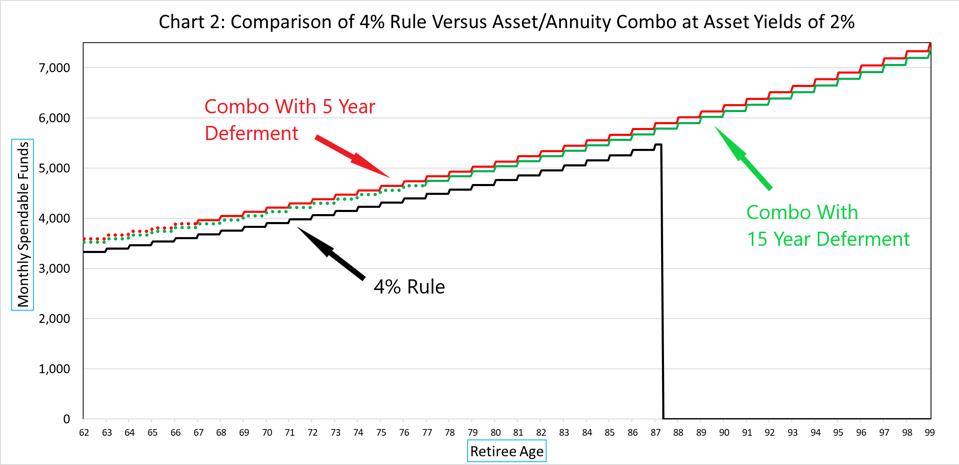

Chart 2 uses the 2% yield on assets. This reduces the spread between the deferment periods, but both remain higher than the 4% rule through age 88. At that point, the 4% rule runs out. Further exploration indicates that a yield of 4.75% is needed to retain payments under the 4% rule through age 104.

MORE FOR YOU

www.mtgprofessor.com

Note that monthly draw amounts are the sole criteria used to compare the 4% rule with combos. Estate values, which are larger with the 4% rule under high asset return assumptions, are ignored. Retirees using the combo should either be indifferent to their estate value, or set aside some of their assets for it.